All Categories

Featured

Table of Contents

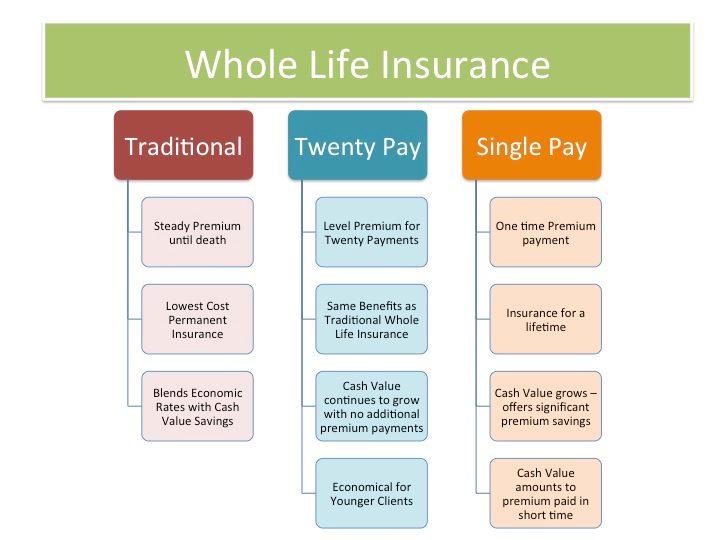

The are entire life insurance coverage and global life insurance coverage. The cash money value is not included to the death advantage.

After ten years, the cash value has grown to around $150,000. He secures a tax-free funding of $50,000 to begin a service with his sibling. The policy lending rate of interest is 6%. He pays off the finance over the following 5 years. Going this path, the rate of interest he pays returns into his policy's cash worth as opposed to an economic institution.

Infinite Bank

Nash was a money specialist and follower of the Austrian institution of business economics, which promotes that the value of products aren't clearly the outcome of traditional financial structures like supply and need. Instead, individuals value cash and products differently based on their economic status and requirements.

Among the mistakes of traditional banking, according to Nash, was high-interest rates on lendings. A lot of people, himself included, entered into economic trouble due to dependence on financial institutions. As long as banks established the rates of interest and car loan terms, people really did not have control over their very own riches. Becoming your own lender, Nash established, would place you in control over your monetary future.

Infinite Financial requires you to possess your economic future. For goal-oriented individuals, it can be the finest monetary device ever. Right here are the benefits of Infinite Financial: Probably the solitary most advantageous element of Infinite Banking is that it improves your money flow.

Dividend-paying whole life insurance is extremely reduced risk and uses you, the insurance holder, a good deal of control. The control that Infinite Banking offers can best be grouped right into 2 categories: tax benefits and asset protections - how do i start infinite banking. One of the reasons whole life insurance is suitable for Infinite Banking is how it's tired.

Nelson Nash Infinite Banking Book

When you utilize whole life insurance policy for Infinite Banking, you become part of a personal contract between you and your insurer. This personal privacy provides particular asset securities not found in other financial vehicles. These protections might differ from state to state, they can include defense from property searches and seizures, security from reasonings and security from financial institutions.

Entire life insurance coverage policies are non-correlated properties. This is why they function so well as the economic foundation of Infinite Financial. Regardless of what takes place in the market (supply, actual estate, or otherwise), your insurance policy preserves its worth.

Entire life insurance policy is that 3rd container. Not just is the price of return on your whole life insurance coverage plan guaranteed, your fatality advantage and premiums are additionally ensured.

Below are its main benefits: Liquidity and ease of access: Policy fundings supply immediate access to funds without the constraints of standard financial institution lendings. Tax efficiency: The money worth expands tax-deferred, and policy financings are tax-free, making it a tax-efficient tool for constructing wealth.

Infinite Banking Agents

Property security: In several states, the money value of life insurance policy is protected from lenders, adding an additional layer of monetary security. While Infinite Financial has its qualities, it isn't a one-size-fits-all solution, and it includes significant downsides. Right here's why it may not be the most effective approach: Infinite Financial often requires detailed plan structuring, which can perplex insurance policy holders.

Think of never ever having to fret about small business loan or high interest prices once again. What happens if you could obtain cash on your terms and build riches at the same time? That's the power of boundless financial life insurance policy. By leveraging the cash money worth of whole life insurance IUL plans, you can expand your wide range and obtain money without depending on standard banks.

There's no set financing term, and you have the freedom to determine on the payment schedule, which can be as leisurely as repaying the lending at the time of death. This adaptability includes the servicing of the finances, where you can select interest-only repayments, keeping the car loan balance level and workable.

Holding cash in an IUL repaired account being credited rate of interest can usually be better than holding the cash money on deposit at a bank.: You've always imagined opening your very own pastry shop. You can borrow from your IUL policy to cover the first expenditures of renting a space, buying equipment, and hiring staff.

Infinite Banking Powerpoint Presentations

Individual lendings can be gotten from conventional financial institutions and lending institution. Right here are some key factors to consider. Debt cards can supply an adaptable way to borrow cash for extremely short-term durations. Nonetheless, borrowing cash on a credit report card is generally really costly with interest rate of passion (APR) often reaching 20% to 30% or more a year.

The tax treatment of plan loans can differ substantially depending upon your nation of residence and the details regards to your IUL plan. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, policy loans are generally tax-free, using a considerable benefit. In various other territories, there might be tax obligation effects to take into consideration, such as potential tax obligations on the loan.

Term life insurance coverage only gives a survivor benefit, with no money worth buildup. This implies there's no cash money worth to borrow versus. This article is authored by Carlton Crabbe, Chief Executive Policeman of Capital permanently, a specialist in offering indexed universal life insurance policy accounts. The information offered in this article is for educational and educational purposes only and need to not be taken as economic or investment guidance.

However, for finance officers, the extensive laws imposed by the CFPB can be viewed as cumbersome and restrictive. Funding officers usually say that the CFPB's laws produce unneeded red tape, leading to more documentation and slower lending processing. Regulations like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) requirements, while focused on protecting customers, can result in delays in closing bargains and boosted operational prices.

{kind=link}

Latest Posts

Be Your Own Bank

The Infinite Banking System

Infinite Banking Concept Pros And Cons